Business Financial Ratios Every Owner Should Understand Before a Sale or Financing

A financial ratio is a single calculation, drawn from the income statement or balance sheet, that buyers, lenders, and acquirers use to read business health and risk. The ratios in this guide are the ones that come up most often in sale processes and lender conversations. They are the most consequential numbers in the business that owners did not pick, and the ones a third party will scan in minutes to decide whether to make an offer, approve a loan, or pass.

Owners already know revenue and rough profit margin. Most have not spent time thinking about leverage ratio, working capital coverage, or the gap between EBITDA and free cash flow. Those are the numbers that drive offer structures, lender terms, and the haircut a buyer applies to a headline multiple. Understanding them in advance is the difference between explaining a business and reacting to someone else's interpretation of it.

This piece walks through the ratios that come up most often in sale processes and lender conversations, with the benchmarks buyers use and what each one signals.

Ratios at a Glance

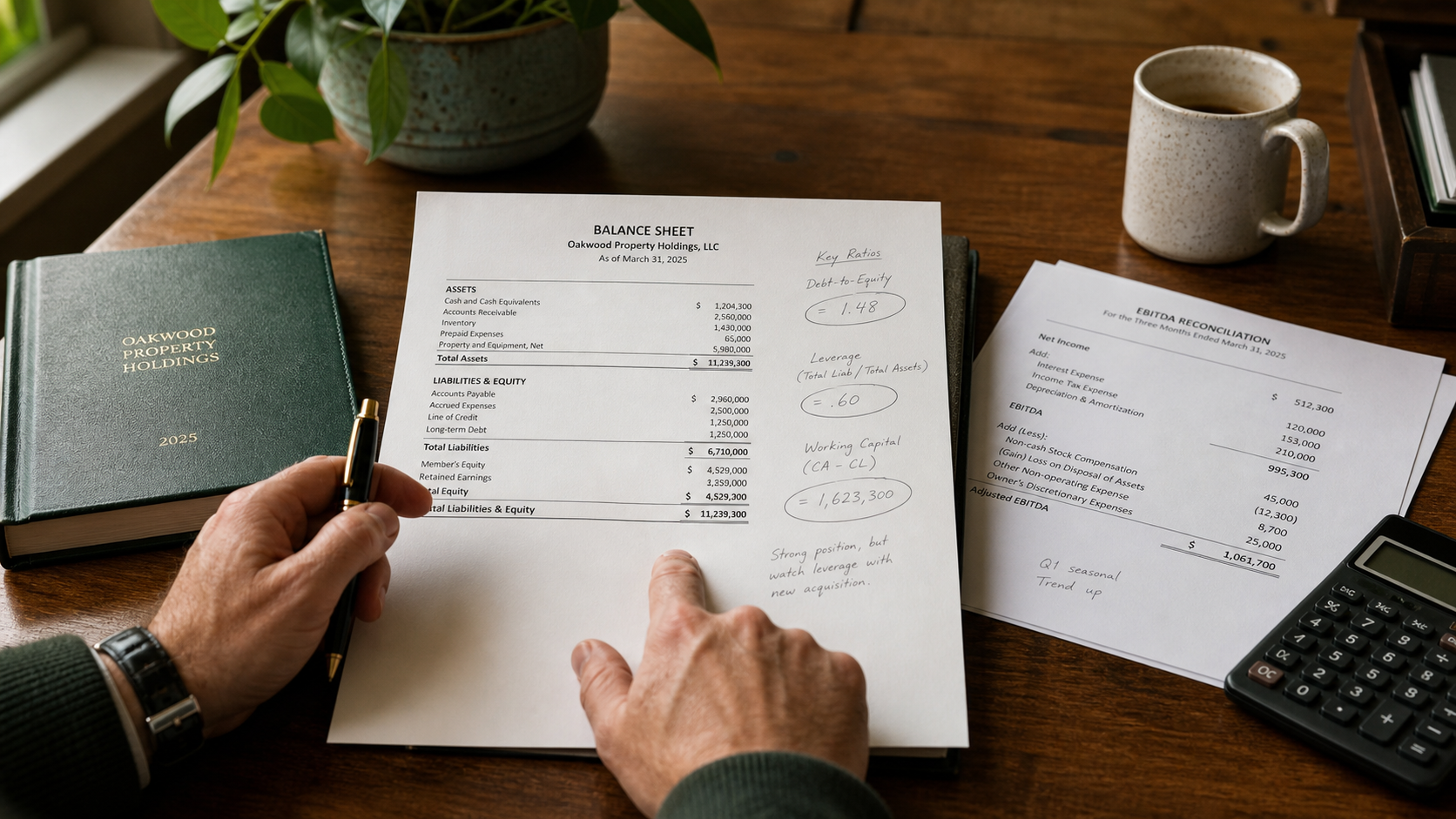

- Debt-to-Equity (Total Liabilities ÷ Total Equity). Typical 1.0 to 2.0. A strong number signals manageable leverage and room for acquisition debt.

- Leverage / Debt-to-EBITDA (Total Debt ÷ EBITDA). Below 3.0x preferred by lenders. Signals conservative leverage and easier financing.

- Working Capital (Current Assets minus Current Liabilities). Current ratio of 1.2 to 2.0 is generally acceptable. Signals short-term solvency.

- Free Cash Flow (Operating Cash Flow minus Capital Expenditures). Consistent positive FCF is the strongest signal of business health.

- Asset Turnover (Net Revenue ÷ Average Total Assets). 0.5 to 2.0, varies by industry. Signals capital efficiency.

- Inventory Turnover (COGS ÷ Average Inventory). 4 to 12x, varies by industry. Signals lean operations and demand alignment.

- Debt-to-Income / DTI (Monthly Debt ÷ Gross Monthly Income). Below 43 percent is the SBA threshold for loan eligibility.

The P/E ratio appears in financial media constantly and is primarily a public market metric. For closely held businesses, the analogous concept is the EBITDA multiple, which we cover below.

Leverage Ratio (Debt-to-EBITDA): The Metric Lenders and PE Use Most

Formula: Total Debt ÷ EBITDA

This is the single most common leverage metric in middle-market M&A and acquisition financing. Lenders typically prefer below 3.0x. Private equity often targets 3.0x to 5.0x depending on industry and deal structure. Above 5.0x, the business becomes difficult to finance through conventional channels.

A worked example. A business with $1.5M in EBITDA and $3M in total debt carries a 2.0x leverage ratio, well within bankable range. The same business at $6M in debt carries a 4.0x ratio, still acquirable but likely requiring a larger equity contribution from the buyer or seller financing to make the math work.

The denominator is the lever that matters most here. Adjusted EBITDA with disciplined add-backs determines how much debt the business can support. Get the EBITDA wrong, and the leverage ratio is fiction. Owners who understand their leverage position before an offer arrives can explain it on their own terms. Owners who do not get the explanation from a buyer's analyst instead.

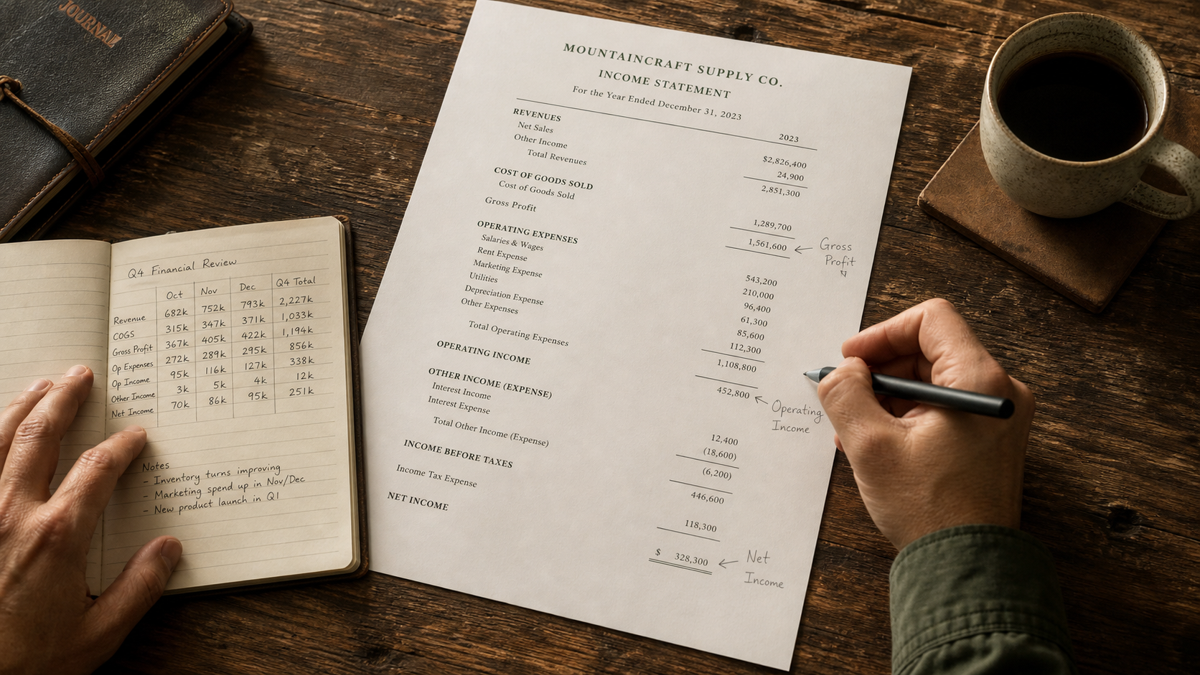

Free Cash Flow: The Most Honest Number in the Business

Formula: Operating Cash Flow − Capital Expenditures

Free cash flow is the closest thing to truth on a closely held P&L. It accounts for what EBITDA leaves out: working capital changes, the real cash cycle, and the capital reinvestment the business requires to stay where it is. A business with $800K in operating cash flow and $200K in annual capex generates $600K in free cash flow. That is the cash available to service debt, distribute to owners, or reinvest for growth.

Strategic buyers and private equity firms use FCF to stress-test valuation. If FCF sits well below EBITDA, the business is capital-hungry or working-capital-intensive, and buyers will haircut the EBITDA multiple accordingly. A $1.5M EBITDA business valued at 6x looks like a $9M deal. If FCF is only $700K because of reinvestment needs, the implied return on the buyer's capital changes, the financing changes, and the offer changes.

Consistent positive FCF across multiple years is the single strongest indicator of business health and sustainability. Buyers pay premiums for businesses that generate reliable cash without constant owner intervention, because that is what transferable value looks like in practice.

Working Capital: The Number That Will Appear in the Purchase Agreement

Formula: Current Assets − Current Liabilities. Current ratio = Current Assets ÷ Current Liabilities, with 1.2 to 2.0 generally acceptable.

What most owners do not realize until they are deep in a deal: most business sale agreements include a working capital target, often called a "peg." It is the agreed level of net working capital the seller must deliver at closing. Shortfalls are deducted from the purchase price dollar for dollar. Surpluses may be retained by the seller or paid out as an adjustment.

A worked example. If the working capital peg is $600K and the business delivers $480K at close, the seller takes a $120K reduction in proceeds. That is not a rounding error. It is a structural mechanism many owners discover only when they try to draw down receivables or defer payables in the final weeks before closing.

SBA and acquisition lenders also require positive working capital as part of loan approval criteria. A business with chronically negative working capital is harder to finance, which narrows the pool of qualified buyers and shapes the offers that do arrive.

Debt-to-Equity Ratio: How Much of the Business Is Built on Borrowed Money

Formula: Total Liabilities ÷ Total Shareholders' Equity

This ratio tells buyers how much of the business has been built on debt versus retained earnings and owner capital. A range of 1.0 to 2.0 is commonly acceptable across industries. Capital-intensive businesses such as manufacturing and logistics may run higher and still be viewed favorably. Service businesses should trend lower. A D/E above 3.0 to 4.0 starts to concern buyers because it signals limited flexibility to absorb acquisition-related debt or fund post-close investment.

A high D/E ratio does not automatically kill a deal. It changes the conversation. It can suppress the multiple a buyer is willing to pay, and it often creates dollar-for-dollar adjustments to the purchase price, because the buyer's default assumption is that debt follows the balance sheet unless negotiated otherwise.

The Other Ratios in Brief

Three more ratios come up often enough to warrant a mention, even when they sit behind the headline numbers in a sale process.

Asset turnover (Net Revenue divided by Average Total Assets) measures how hard the assets are working. Industry context is everything. Manufacturing typically runs 0.5 to 1.0. Service businesses often run 2.0 or higher. A declining asset turnover over multiple years warrants explanation during due diligence.

Inventory turnover (COGS divided by Average Inventory) signals demand alignment and working capital efficiency. Retail typically runs 12 to 15x, manufacturing 4 to 8x, wholesale and distribution 6 to 10x. Slow-moving inventory may need to be written down or excluded from the deal entirely, which directly reduces the working capital peg.

Debt-to-income (Monthly Debt divided by Gross Monthly Income) is primarily a lender metric. The SBA's general threshold is 43 percent or below for loan eligibility. The ratio becomes especially relevant in management buyouts and internal succession, where the incoming buyer's DTI affects whether the deal can close at all.

How to Read These Numbers Together

No single ratio tells the story. They tell a coherent story only when read together.

Three patterns illustrate the point.

Stretched and slowing. High leverage above 4.0x Debt-to-EBITDA, low free cash flow, and declining asset turnover. The balance sheet is stretched without matching gains in operational efficiency. Difficult to finance, difficult to sell at a strong multiple.

Clean and acquirable. Low leverage, strong inventory turnover, healthy working capital. A well-capitalized, operationally lean business. Lenders say yes quickly. Buyers compete for the deal.

Profit without cash. High EBITDA margin paired with weak free cash flow. The business shows accounting profit while consuming cash through working capital needs or heavy capex. Buyers will reconcile the gap and adjust the offer downward. The headline EBITDA multiple does not survive scrutiny.

Most owners have never looked at their financial statements through a buyer's eyes. That is the work of a different season in the business, when the question shifts from running well to presenting well. Running a business and presenting a business for sale are different disciplines, and the second one becomes important when ownership transition enters the picture.

What to Do If the Numbers Are Not Where You Want Them

Most owners reviewing these ratios for the first time will find at least one number that gives them pause. Surprises here are information. The work is figuring out which numbers to act on and which to reframe with industry context.

Three principles are worth holding in view.

Runway matters. Owners who start looking at the financial profile twelve to twenty-four months before a planned exit have real options to improve ratios before a process begins. Paying down debt to reduce leverage, tightening inventory management, building working capital. These are achievable changes with enough runway. The right time to start exit planning tends to be earlier than owners expect.

Some ratios can be fixed, and some need to be reframed rather than fixed. High leverage may call for a deliberate pay-down strategy. A low asset turnover in a capital-intensive industry may need industry context rather than a structural change. Knowing the difference between the two is part of the work.

The narrative matters as much as the number. Buyers form impressions from how owners explain their financials, on top of what the financials show. An owner who can walk a buyer through the working capital cycle or explain an inventory build with clarity signals operational command. That builds confidence in both the business and the transition, and the work to build that narrative belongs to a broader exit planning effort rather than a process moment.

Working With an Advisor Before the Numbers Arrive on a Buyer's Spreadsheet

The financial profile of a business is one of the first things The McFarland Group looks at when working with an owner who is starting to think about a transition. Not because the numbers are bad, but because understanding them before someone else presents them to you changes the conversation.

The McFarland Group has guided more than $3B in business value through ownership transitions, and the financial picture is always part of the work. Our role is to help owners see what the ratios signal, where the gaps are, and what runway exists to address them.

If you are thinking about a sale, a management buyout, or a refinancing in the next few years and would like to understand what your numbers say to a buyer or a lender, that is a conversation worth having before any process begins.

Related posts

Gross Profit, Net Income, and Operating Margin: What These Numbers Mean When You're Thinking About a Sale

How owners of closely held businesses should think about gross profit, net income, and operating margin, and what each number signals to a buyer.

May 19, 2026 · 7 min read

Succession Planning Checklist for Closely Held Businesses

A practical succession planning checklist covering business readiness, personal readiness, leadership readiness, and legal and financial steps. Built for closely held business owners who want to prepare on their terms.

February 12, 2026 · 7 min read

Related Resources

Services

White Papers

A research-based look at why most succession plans fail and what separates the companies that get it right, drawing on data from Vistage CEO peer groups.

Are You Ready to Sell?A checklist of the risks that reduce business value at sale, and what to fix before you go to market.